At this time last year, the theme of our 2025 outlook was overarching uncertainty. A new administration was about to take over in Washington, inflation was coming down but still not on target, an unruly congress was preparing to be sworn in and, although many things had been promised, it wasn’t clear what legislation could actually get passed. Additionally, it was unclear what effect expected executive orders on tariffs and immigration might have on the economy.

Now, headed into 2026, there is a higher level of certainty, which is a good thing on balance. Markets hate uncertainty. However, what we have seen in terms of economic performance is a mixed bag depending on where you look. Many economists are talking about a K-shaped economy and we believe it is a good description. We are expecting more of the same in the new year.

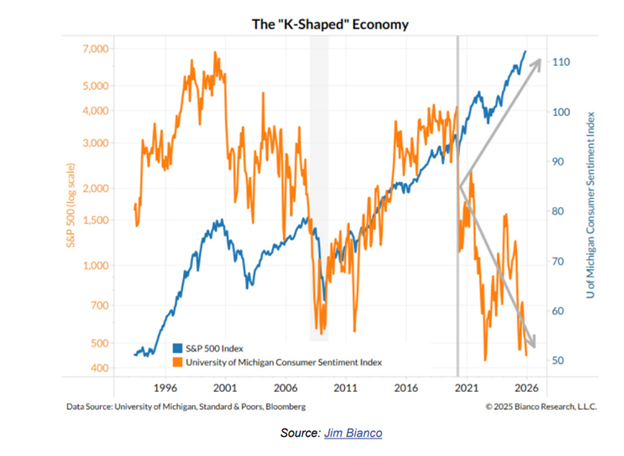

What is a K-shaped economy? The k-shape comes from two divergent components of the economy that have historically trended together or would be expected to track a similar path. Courtesy of Bianco Research, Jim Bianco offers this chart showing the positive trending S&P 500 and the negative trending University of Michigan Consumer Sentiment index.

You can see the two series of data have tracked more or less together until something happened in 2021. At that point, the correlation broke and the two series have moved in opposite directions. And there are many of these sorts of relationships that can be seen across a wide spectrum of the current economic landscape. These include the labor market, where large companies have mostly been able to maintain or grow their workforce but mid and smaller companies have suffered layoffs and labor shortages, investment in AI infrastructure has ramped up exponentially while investment in traditional manufacturing has languished, services sector revenue continues to beat expectations and multiple goods sector revenue continues to fall quarter after quarter. These divergent pathways even can be seen on the Federal Reserve’s Open Markets Committee where views have the committee split on whether weakness in the labor market or the threat of an uptick in inflation is the larger risk.

All of these diverging trends have led to an economy that shows uneven progress. We expect that will continue to be the hallmark of the coming year. As a consequence, we believe diversification is of even greater importance than usual. These relationships could unexpectedly snap back to more historical trend lines or could persist for much longer. Additionally, we believe there has been a fundamental shift in the way the government and big tech interact with the economy that further argues for increased diversification. Our friends at Confluence have dubbed it the “techno-industrial state.”

Starting back in the Biden administration, the federal government began to move toward a more interventionist role in business both with the CHIPs Act and the Inflation Reduction Act that were designed to support the semi-conductor and green energy industries through subsidies and loans. That has been followed by the Trump administration 2.0 taking various interventions like a golden share in US Steel, a 10% stake in Intel Corp., revenue percentages of 15% to 25% of chip sales in China from AMD and Nvidia, and a host of direct stakes in numerous rare earth and mining companies. The argument is these are strategic industries that deserve support from government agencies and the defense department.

This is not the first time the federal government has been so intimately involved with US businesses but it is something we have not seen for many decades. The results could be unpredictable as the primary concern of management in these industries might not always be the interest of shareholders in any given situation.

Another trend we will be watching in 2026 is the direction of the Fed and what will happen with interest rates. Fixed income has seen increased inflows in the last half of this year and we expect that to continue based on two assumptions. Starting with the Fed, the market is currently pricing in two or three rate cuts for 2026. Chair Jay Powell will be replaced in May and the most likely replacement will be much more dovish. Will the new chair be able to convince the rest of the committee to go along with more and/or larger rate cuts? This is a key question. We believe it is likely and there is a good chance the fed funds rate could go lower than what the market is pricing in currently. Secondly, as rates go down, the returns on money market and other cash equivalents begin to look much less attractive compared to other fixed income classes. This argues for moving out to slightly longer maturities and duration and finding higher quality credits like asset backed and upper tier investment grade bonds.

We have mentioned the outsize importance of diversification we believe is a key to addressing the challenges of 2026. With just a handful of trading sessions left in the current year, the major US stock indices will very likely finish with decent, double-digit annual gains. However, when you look under the hood, the best performing asset classes are emerging markets and foreign developed stocks. US growth and large caps will likely finish the year almost 10% below those leaders followed by small caps, commodities, value stocks and mid-caps. Interestingly, over the last 3 months, and especially over the last month, the Russell 2000 small cap index has outperformed the S&P 500. This widening of market breadth is a healthy sign and is likely to continue in the new year. It’s a trend we will be watching closely and is one of the reasons we argue for solid diversification across asset classes and sectors.

Another important trend to follow as the calendar rolls over is the massive runup in AI infrastructure spending. At the moment, the demand for AI computational capacity far outstrips supply. The two essential infrastructure components are advanced microchips and the data centers that house the computers that run them. Additionally, you need lots of electricity to power the whole operation. This is why “compute” or capacity is normally measured in megawatts. Over the last two decades, just 4 companies, known as the hyperscalers, have built and operate over a third of all data center capacity. This is set to drastically change as new players enter the market. During 2025, we seemed to have weekly, if not daily, announcements of new deals to add hundreds of gigawatts of capacity from not only the hyperscalers, but finance entities, hedge funds, chip suppliers, individual entrepreneurs and even countries. And one couldn’t help but scratch one’s head at the circular nature of some of these deals. And there have already been a couple of spectacular blow ups where a deal has been announced but the reality of final user demand seems to call into question the massive capital expenditure. The key to success for this investment will be getting final user demand but the risk of overcapacity is not insignificant.

Finally, we can’t forget that 2026 is an election year. That should add some additional spice to what is already an interesting set up. We’ll be here for it. Happy New Year!

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.